It is well known that energy efficiency investments provide opportunities to reduce energy costs and opportunities to leverage incentive dollars. As we have discussed recently in this blog, the relative attractiveness of energy efficiency investments may be evaluated in terms of first cost, simple payback, and life cycle cost. But for a given investment alternative, is it advantageous to finance?

Financing (Photo credit: LendingMemo)

Financing (Photo credit: LendingMemo)Financing example

Financing inevitably brings added costs to an investment, notably borrowing costs that are quantified by a loan interest rate. If financing costs more, why bother? Well, if first costs and payback periods are important considerations for your investments, consider the following example.

Investment Capital Cost: $100,000

Annual Energy Savings: $20,000

Financing Down Payment: $50,000

Financing Interest Rate: 5%

Faster cash flow payback

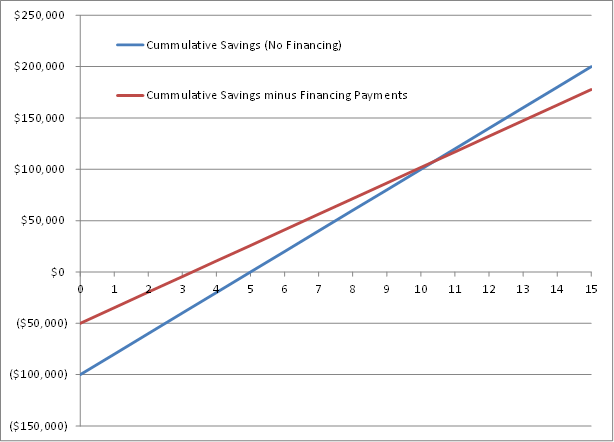

In this example, the simple payback is 5 years (without financing). If the investment is financed according to the terms listed, and if the loan is repaid over 15 years in equal payments, the payback period is less than 3.5 years. Figure 1 below shows the cumulative cash flows for non-financed vs. financed investment. We can see that the financed investment accumulates less total savings at the end of the 15 year lifetime (due to borrowing costs); nevertheless, the first cost is less and the payback is faster.

Figure 1: Cumulative cash flows for non-financed vs. financed investment.

The payback will be faster with financing if the non-financed internal rate of return (IRR) is higher than the loan interest rate. In the example above, the IRR is 18 percent which is substantially higher than the 5 percent interest rate for the loan.

The added benefit of efficiency incentives

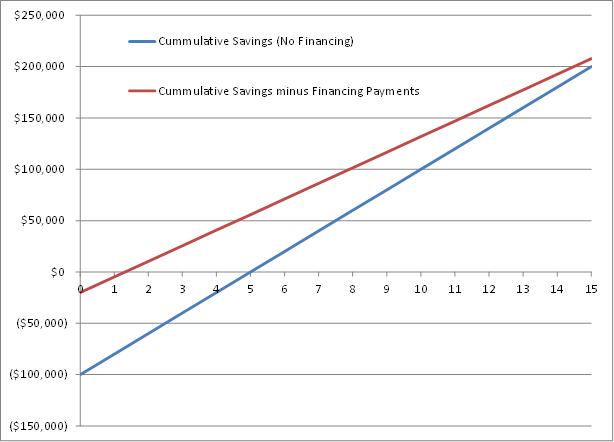

If we include efficiency incentives that buy-down the capital cost of the investment, then the payback will be even faster. Up-front incentives can even be enough to offset the borrowing costs of financing. Figure 2 shows the cumulative cash flows for non-financed vs. financed investment, where the financed investment includes a rebate incentive of $30,000. In this example, the 30 percent rebate on the $100,000 investment with financing (50 percent down payment and 5 percent interest rate) provides a less than 1.5 year payback and a lower life cycle cost for the investor. Rebates plus financing can deliver very attractive investment opportunities, in terms of first cost, payback period, and life cycle cost. Creative public financing, such as the NY Green Bank, are making these opportunities possible for savvy, energy-conscious investors.

Figure 2: Cumulative cash flows for non-financed vs. financed investment (with rebate incentive).